Enodo Untangled

Enodo Untangled

- Array of US rules aim to block China’s tech ambitions

- Explicit US aim is to keep big tech lead

- Curbing China’s access to advanced chips a US priority

- US seeks to slow China’s march to becoming an AI power

- US gets Netherlands, Japan to join tech embargo

- China will struggle to make top-end chips on its own

- No China retaliation against US firms, for now

- Next US targets may be quantum computing, biopharma

- China rattled by US campaign but retains its ambitions

Executive summary

America is refreshingly direct in describing the strategic goal of the high-tech war it is waging against China. It is no longer enough to keep a relative edge over its competitors but, “given the foundational nature of certain technologies”, to maintain as large of a lead as possible, according to National Security Adviser Jake Sullivan.

The competitor-in-chief is China and the principal technologies at stake are advanced logic and memory chips that are critical, among other things, to the development of artificial intelligence applications.

The impact of the administrative and legislative weapons that Washington is brandishing in its war is the topic of this Enodo Untangled. The array of measures is as sweeping as America’s strategic aim. More than 600 companies are in effect barred from doing high-tech business with China, while the Netherlands, Taiwan, South Korea and Japan have been enlisted as auxiliaries in the US campaign.

In response to the sanctions, Beijing is doubling down on efforts to upgrade its domestic chip-making industry, but we conclude that it will be hard for China to replicate the technology and supply chains required to make advanced semiconductors. Chinese firms are not the only casualties. Western tech companies with operations in China are also caught in the crossfire, wary both of incurring US displeasure and of inviting possible Chinese retaliation.

Given that anti-China feelings are running high on both sides of the aisle in Congress, the outcome of next year’s US presidential election is unlikely to lead to a de-escalation of the tech war. Indeed, Washington may decide to extend hostilities to two other critical technologies: quantum computing and biopharma.

For its part, China under Xi Jinping remains determined to become a technological superpower and to use that power in its national interest. Just as the US has done for years. The battle lines are drawn.

Trump starts the Tech War

In 2018 the Trump administration fired the first shots in what has become a growing effort to constrain China’s ability to achieve global dominance in areas of advanced technology critical for national security and national advantage. Washington initially focused on preventing China from becoming a global leader in the provision of fifth-generation (5G) mobile technologies through its national telecommunications champions Huawei and ZTE.

The 5G issue epitomised the dilemma facing the US: 5G relied on technologies developed in the US but manufactured elsewhere.

As a consequence no US company had the manufacturing or systems integration skills to produce a commercially viable end-to-end 5G network in the way that China could. The US response was to strongarm allies into excluding Huawei from their 5G networks while imposing an embargo on exports of advanced semiconductors to Huawei.

This approach had mixed results and the long-term impact on Huawei’s business remains to be seen. The company’s mobile phone business was destroyed but Huawei has continued to provide 5G networks within China and overseas, predominantly though not exclusively in the developing world.

![]()

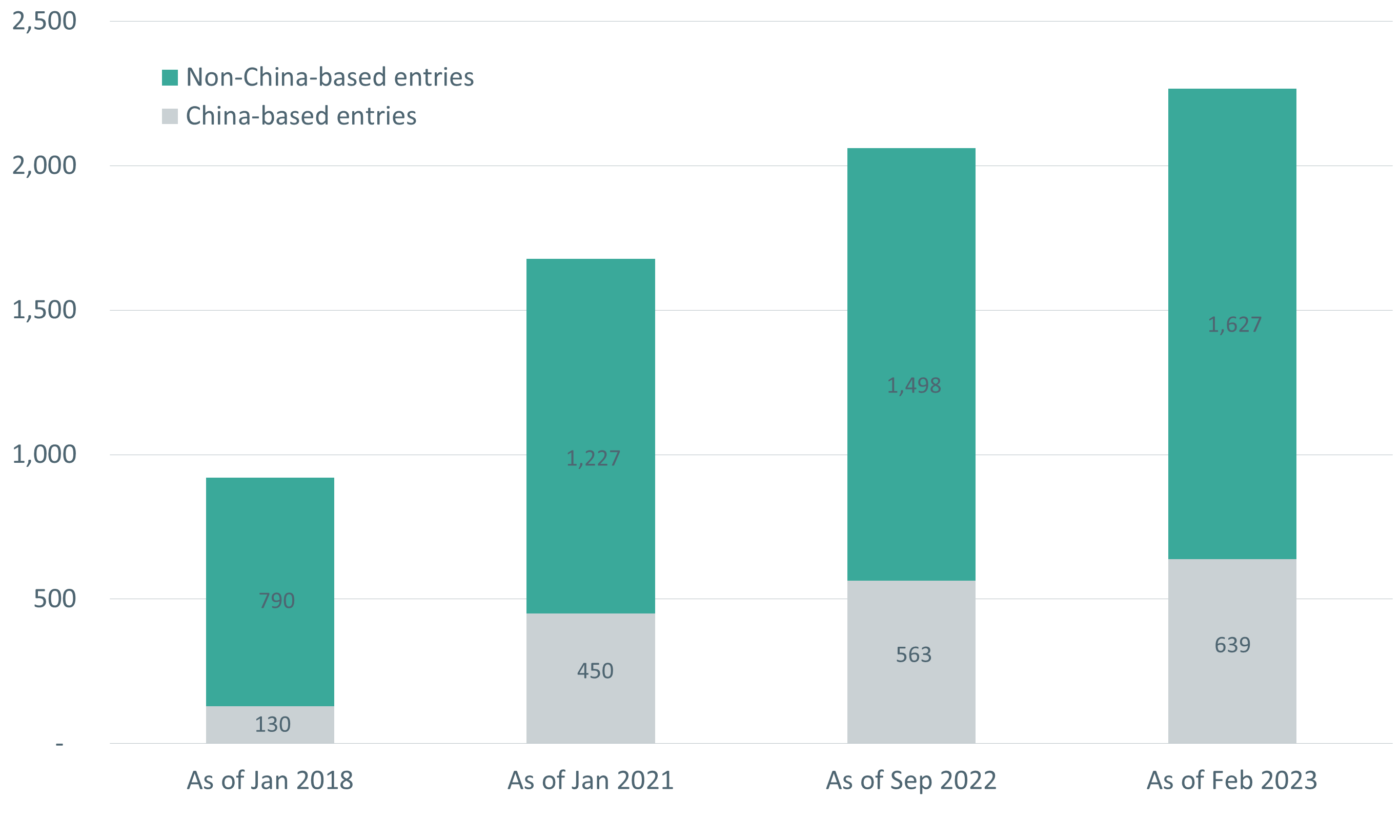

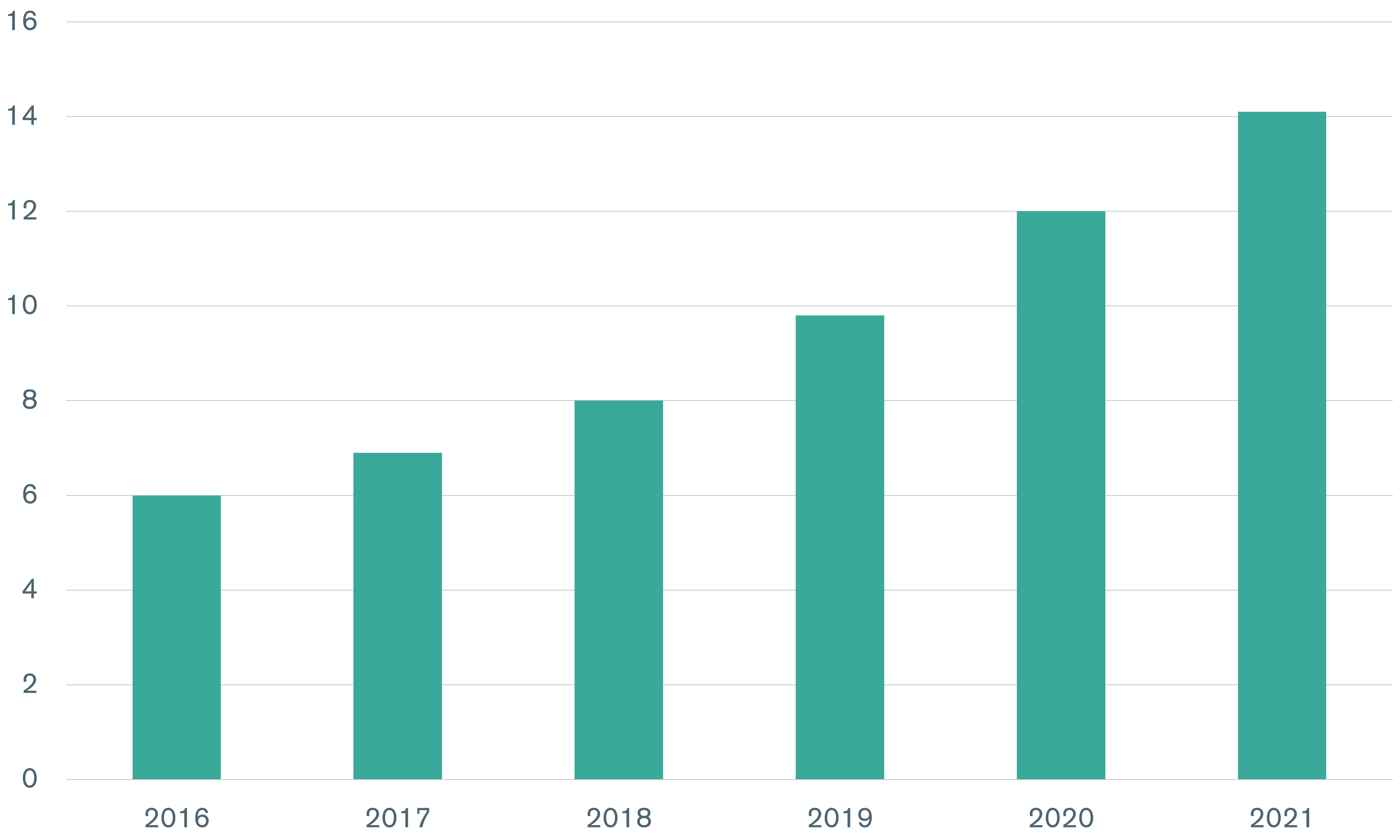

The attack on Huawei was accompanied by other measures, including adding more Chinese technology companies to the Department of Commerce’s Entities List. This list was first compiled in 1997 to prevent US technology being used in the proliferation of weapons of mass destruction but was subsequently expanded to include activities detrimental to US national security. There are currently 600 Chinese companies on the Entities List on the basis that they are believed to be engaged in military-related research projects.

![]()

![]()

The Foreign Direct Product Rule, introduced in 1959 to prevent the sale of technology with more than a specified proportion of US technology, and which has extraterritorial application, was applied more rigorously. So were the rules of the Committee on Foreign Investment in the US (CFIUS) aimed at restricting China’s ability to obtain US IP through the acquisition of US companies. And visa restrictions were imposed on Chinese graduate students identified as having connections to Chinese civil-military fusion programmes.

A more focused strategy under Biden

Like much else about the Trump administration, efforts to contain China’s technical progress were somewhat inchoate and piecemeal. But by the autumn of 2022 the Biden administration had developed and articulated a more structured and strategic approach with the same end in view. This approach was trailed by National Security Adviser Jake Sullivan in a September 2022 address to the Special Competitive Studies Project set up by former Google chairman Eric Schmidt to determine how the US could maintain a scientific and technical edge over China.

Sullivan made himself clear: ”We have to revisit the longstanding premise of maintaining ‘relative’ advantages over competitors in certain key technologies.

We previously maintained a ‘sliding-scale’ approach that said we need to stay only a couple of generations ahead. That is not the strategic environment we are in today. Given the foundational nature of certain technologies, such as advanced logic and memory chips, we must maintain as large of a lead as possible.”

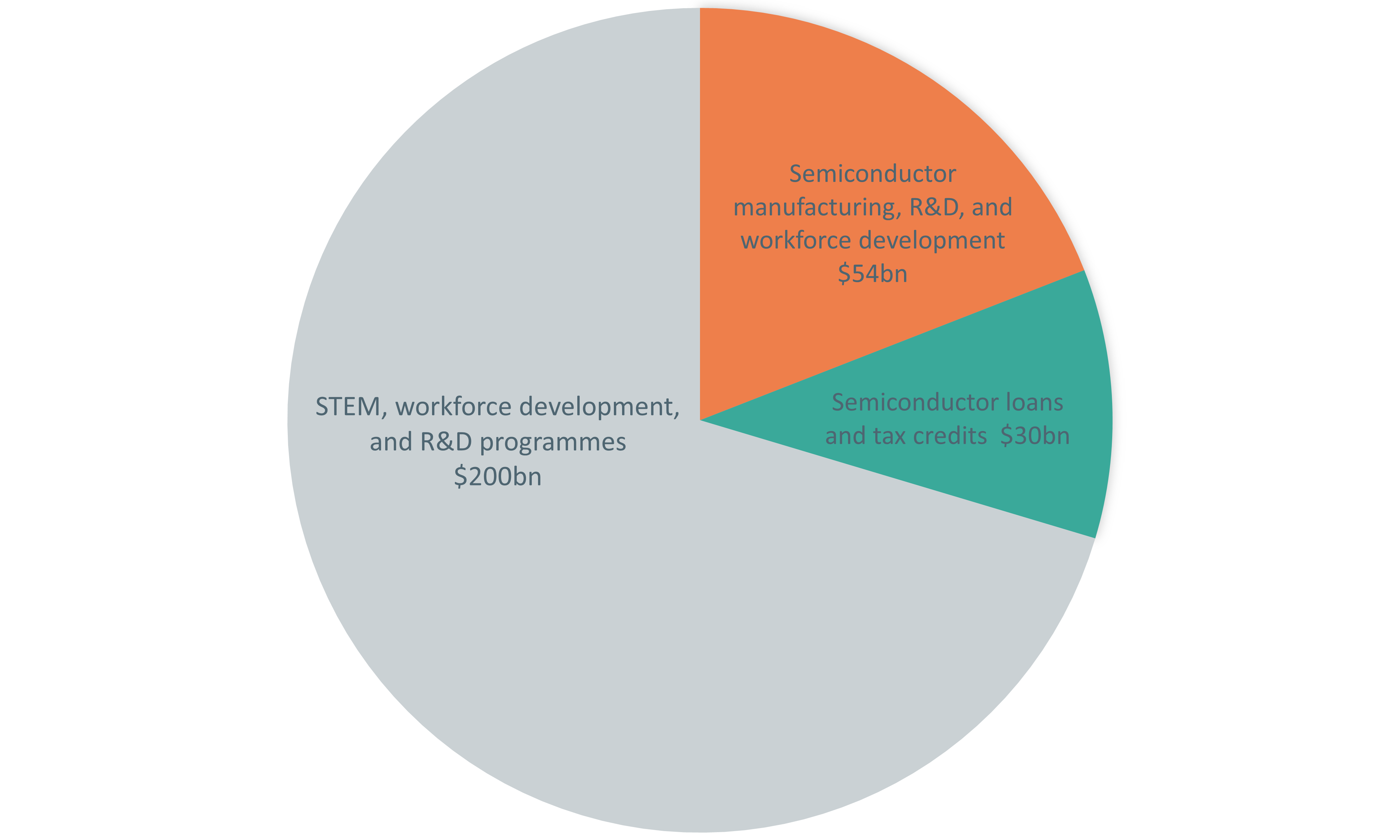

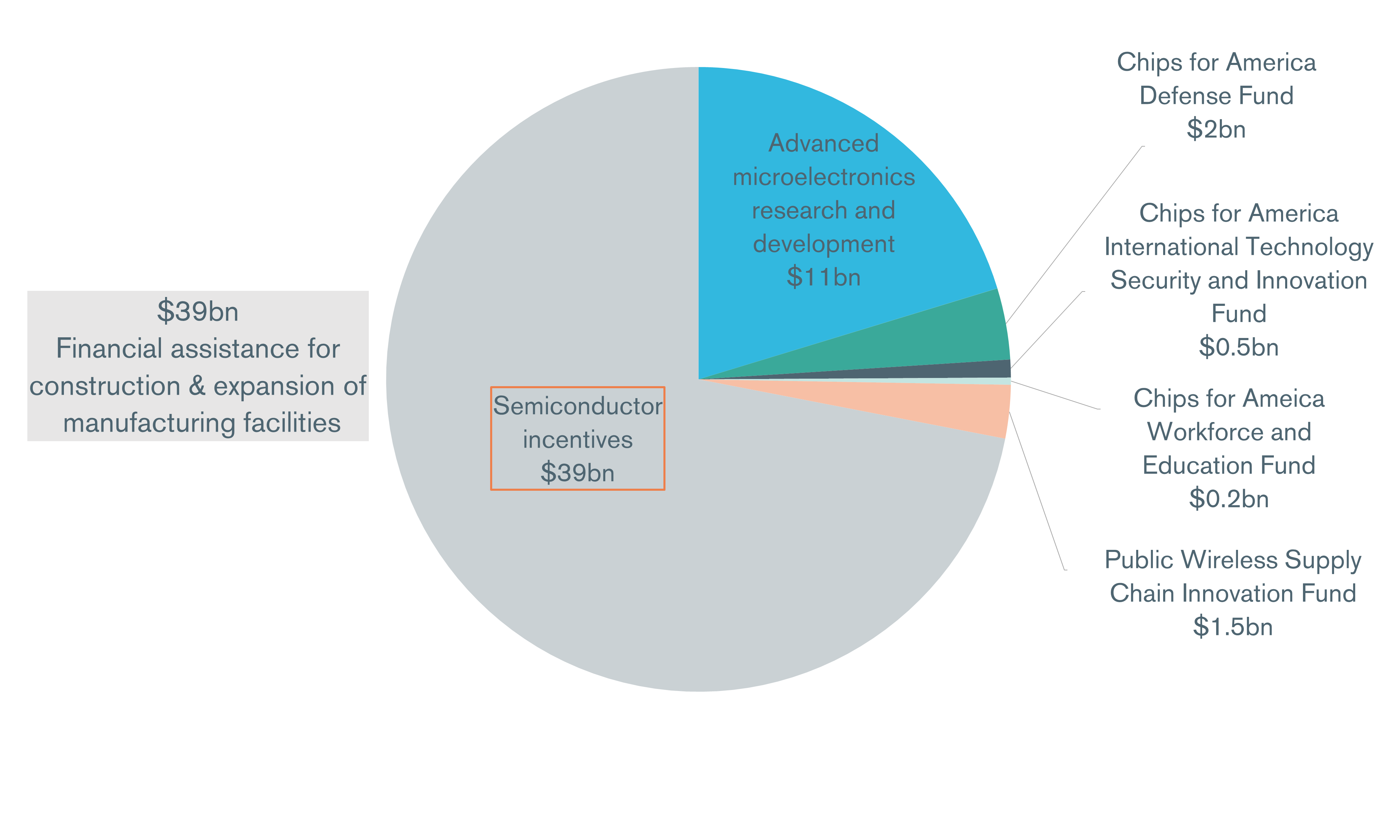

By this stage the Biden administration had already passed into law the CHIPS and Science Act 2022, aimed at encouraging a renaissance in US domestic hi-tech manufacturing. The Act provides for $280bn in spending over the next 10 years. The majority — $200bn — is for scientific R&D and commercialisation.

![]()

The $54.2bn in the CHIPS Act is for semiconductor manufaturing, R&D and workforce development, and finally, another $6bn for loans and $24bn worth of tax credits for chip production.

![]()

Under the Act, any company in receipt of funding to establish facilities in the US will be barred from investing in technology projects in China for 10 years. Those with existing factories in China will be barred from expanding output by more than 5% over the same 10-year period – though this does not apply to production gains achieved through technology innovation.

The practical application of the approach outlined by Sullivan became clear the following month when the Department of Commerce’s Bureau of Industry and Security issued new rules restricting the sale of advanced semiconductors to Chinese entities and the equipment needed to make them.

The rules restricted specifically the sale of logic chips with non-planar transistor architectures (i.e. FinFET or GAAFET) of 16 nanometres or 14nm, or below; dynamic random-access memory (DRAM) chips of 18nm half-pitch or less; and NAND flash memory chips with 128 layers or more.

In effect, the US government was not only making it impossible for China to acquire or manufacture semiconductors at the most advanced production nodes but also making it significantly harder for the country to maintain existing production at less advanced nodes.

The new regulations targeted in particular the sale of advanced graphics processing units (GPUs) needed to train large language model (LLM) AI programmes and to enable small-scale high-performance computing applications. Specifically, they forbade the sale to Chinese companies involved in civil-military fusion projects of GPUs with a data transfer rate above 600 gigabits per second.

This will limit the ability of sanctioned companies to “train” LLMs and hence impair China’s ambition to become a globally leading AI power.

The new rules also prohibited ‘US persons’ – not merely citizens or green-card holders but anyone resident in the US – from assisting China in the development of advanced semiconductors, a move that resulted in the immediate repatriation of hundreds of US engineers working on projects in China.

The term used by US officials to describe the overall approach was “small yard, high fence”, meaning that restrictions would be applied only to a small subset of critical technologies while trade in technologies not deemed critical could continue unimpeded.

The US restrictions could, however, only be effective to the extent that other key players – Taiwan, Japan and South Korea for semiconductors and the Netherlands for advanced lithography machinery – were willing to implement them.

In order to convince them, the US was at pains to make clear that its embargo extended to technologies in which the US had no competitors – argon fluoride immersion Deep Ultraviolet Lithography, steppers and scanners, electron beam tools and resist processing tools – as a demonstration of its willingness to accept some pain.

These efforts appear to have been broadly successful. The Dutch firm ASML, which has a global monopoly on the production and sale of Deep Ultraviolet (DUV) and Extreme Ultraviolet (EUV) lithography machines needed for making the most advanced semiconductors, had already denied China access to EUV technology under the Wassenaar Arrangement but will henceforth stop selling DUV machines and stop servicing those it has already sold to China.

In private conversations the Dutch government has made clear that it willingly conformed to the new restrictions – though the same cannot be said for ASML, for whom China represents a lucrative market.

On 31 March 2023 Japan added 23 items, including advanced semiconductor manufacturing equipment, to its list of products subject to export controls.

South Korea, whose national semiconductor champions Samsung and SK Hynix have production facilities in China accounting respectively for 40 and 50% of their total output, was granted a one-year waiverfrom compliance with the US restrictions. In any event, much of the output of these companies in China is at the more mature production nodes not subject to sanctions.

Impact on China

The US decision to impose restrictions on sales of advanced semiconductors and the equipment needed to make them targeted a major Chinese vulnerability. Advanced semiconductor manufacturing is the product of decades of incremental improvements and deep technical specialisation. ASML’s DUV and EUV lithography machines have thousands of highly specialised components, many of which were designed in the US. This means that the US government can, through the Foreign Direct Product rule, determine to whom they can be sold.

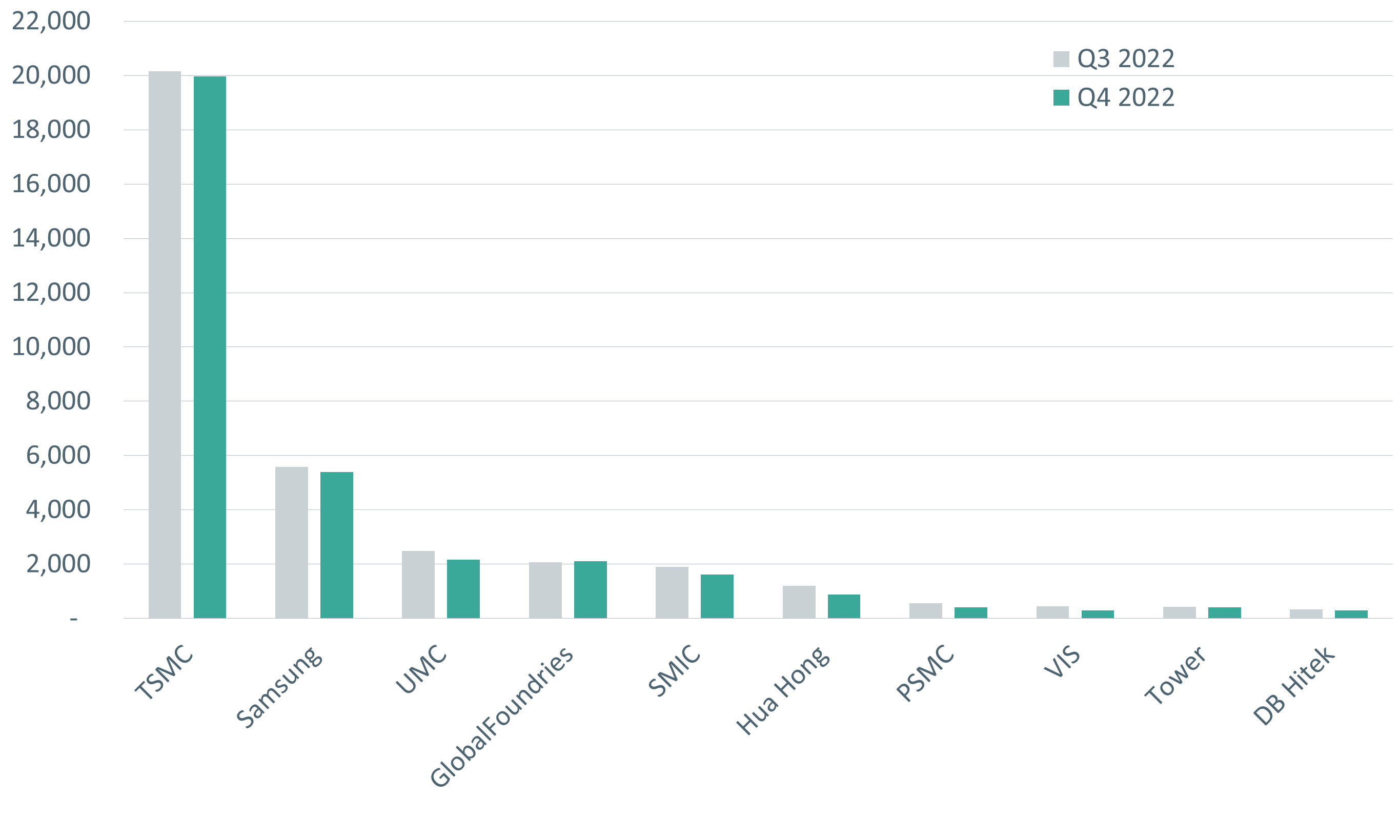

In practice, the most advanced semiconductors are produced by just three companies: Taiwan Semiconductor Manufacturing Corp (TSMC), Samsung and Intel. Of these, TSMC operates “pure play” foundries which only manufacture semiconductors to others’ designs while Samsung is a hybrid operation that makes semiconductors for its own products but also to others’ designs.

Intel is the only advanced semiconductor manufacturer in the US and manufactures only for its own products. By its own recognition Intel has fallen behind the most leading-edge technology.

![]()

The cost of setting up an advanced foundry is in the region of $20bn. But the manufacturing process also requires hundreds of specialised inputs – chemicals refined to the highest levels of purity, lenses, mirrors, valves and pipes manufactured to the highest levels of precision and advanced laser technology possessed only by the US.

Moreover, the design of advanced semiconductors relies on the availability of Electronic Design Automation tools produced only in the US and Japan. All the inputs that make up these complex supply chains come from countries that are liberal democracies and to a greater or lesser extent within the Western camp.

It is hard to see how China can hope to replicate either the technology or the supply chains required to manufacture advanced semiconductors within a purely domestic environment, even supposing the requisite technical expertise were available.

A further complicating factor is that to date research on lithography in China has been largely the preserve of academics rather than engineers.

![]()

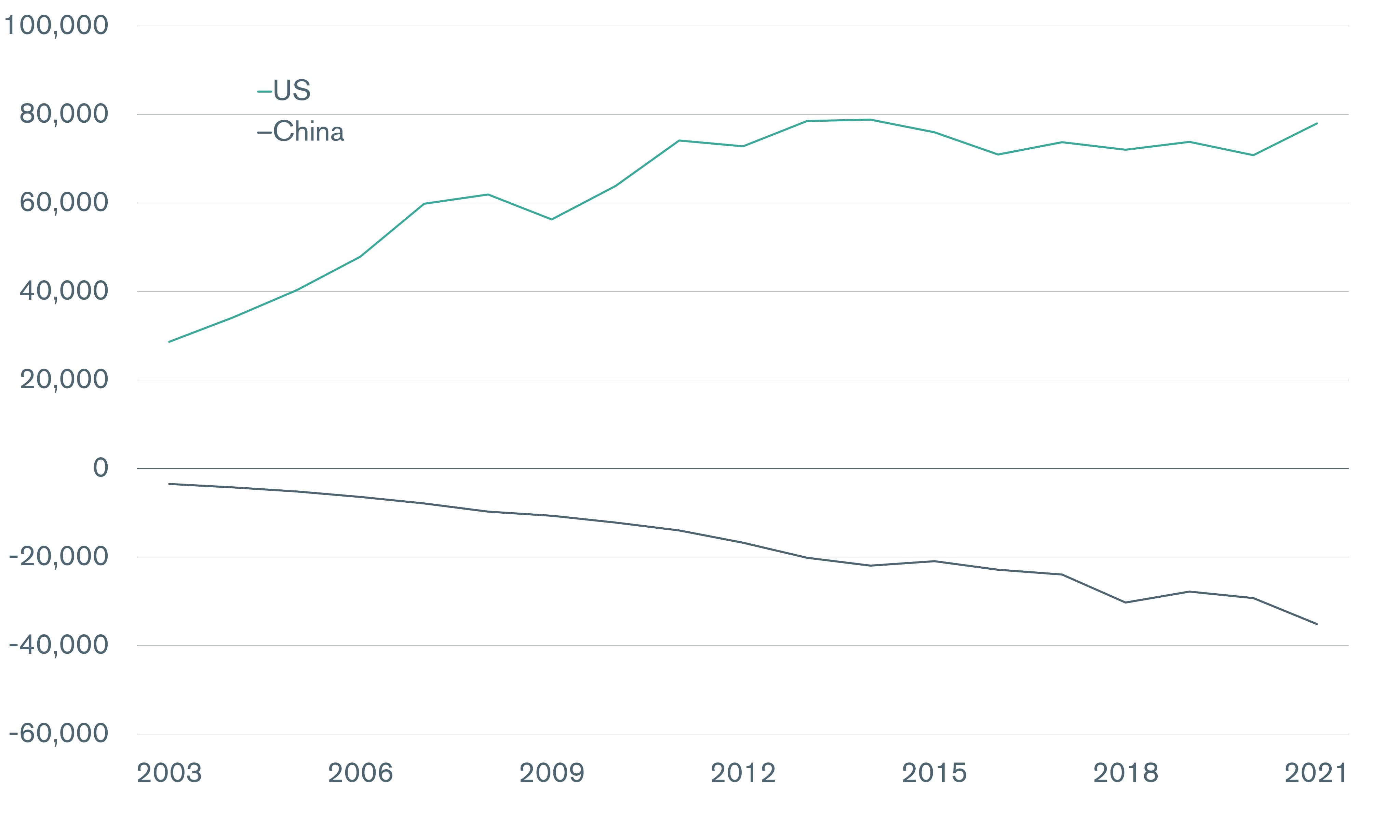

China’s leadership has long been aware of and concerned about China’s reliance on foreign technologies in general and semiconductors in particular. The reasons for this are both economic and geopolitical. China currently spends in the region of $300bn per year on imported semiconductors, much the same amount as it spends on imported oil. In addition, it has to pay substantial sums in royalties to western companies whose technologies it uses.

![]()

The other concern is the geopolitical vulnerability generated by the current dependence. In recognition of this Achilles heel, Beijing set up the China Integrated Circuit Industry Investment Fund, aka the Big Fund, in 2014 with a capitalisation of $40bn to promote domestic semiconductor production. In June 2022 a review conducted by Vice-Premier Liu He confirmed that there was little to show for this investment, and those heading the fund were indicted for corruption.

Facing up to failure – and finding work-arounds...

This failure has been replicated in provinces and municipalities across China, many of which have capitalised start-ups often headed by individuals with no background in the industry. It is impossible to calculate how much money has been wasted on such projects, but the sum certainly extends to hundreds of billions of dollars.

China’s central government has now confronted this failure and, as part of a series of governance reforms enacted at the 2023 Two Sessions, a Central Science and Technology Commission was set up to exercise interdepartmental coordination in the pursuit to technological self-reliance.

Within this framework, a number of national technology champions, including Semiconductor Manufacturing International Corp (SMIC), Hua Hong Semiconductor, Huawei and equipment suppliers NAURA and Advanced Micro-Fabrication Equipment Inc, are to receive subsidies and get more control over state-backed research with no obligation to achieve state-mandated performance goals.

Notwithstanding the apparently swingeing nature of the US restrictions, firms in China have found ways to continue accessing some embargoed US technology.

In anticipation of US actions these companies have stockpiled both semiconductors and manufacturing equipment. The US chipmaker Nvidia has developed A 800 and H 800 GPUs with a data transfer rate of 400 gigabits per second, i.e. low enough to avoid the embargo and still useful for LLM and AI training. Sanctioned companies, including the surveillance national champion iFlytek, have been able to access Nvdia A100 GPUs with a data transfer rate of 600 gigabits by renting access from cloud providers and other companies not subject to restrictions and by purchasing through intermediaries.

...and hitting back

Initially it seemed that China had done virtually nothing to retaliate against the US technology curbs. In recent years China has developed a range of relevant legislation. This includes:

- the Anti-Foreign Sanctions Law, which empowers the Chinese state to seize the assets of entities implementing sanctions against China and imposes liabilities on firms that refuse to help the country counter sanctions;

- an Unreliable Entity List, similar to that of the US;

- and the Rules on Counteracting Unjustified Extra-territorial Application of Foreign Legislation and Other Measures, which bar Chinese persons and companies from complying with extraterritorial applications of foreign laws.

None of these has yet been brought to bear with the exception of the Unreliable Entities List, to which have been added just two US corporations, Lockheed Martin and Raytheon, neither of which does business in China.

But within the past fortnight the Cyberspace Administration of China has launched a cybersecurity investigation into local sales of the US company Micron Technology to “safeguard key information infrastructure supply chain security”.

In view of the fact that Micron has only a small and declining presence in the China market, manufacturing and selling DRAM chips which Chinese companies are able to do and of which China now has a glut, it seems likely that the investigation of Micron should be seen as a signal to other foreign semiconductor manufacturers.

There are also indications that China may be starting to use its Anti-Monopoly Law to block mergers and acquisitions of US tech companies.

Under this law China has to approve any such deal between companies which collectively derive more than $117m a year from the China market. Acquisitions in China’s crosshairs include a projected takeover by Intel of the Israeli company Tower Semiconductors and a takeover by MaxLinear of Taiwan’s Silicon Motion Technology.

China has also intimated that it may ban the export of technology such as furnaces and presses that are needed to process and make magnets out of rare earths critical for the manufacture of wind turbines and electric vehicles.

Such a ban would create difficulties for the US and Western allies. But a recognition that their dependence on China for rare earths was excessive has led to some diversification of suppliers in recent years, so a Chinese ban would not be a killer blow.

More US restrictions are on the way

In addition to semiconductors, the Biden administration has identified other technologies in which the US needs to maintain a strategic edge: quantum computing, bio-pharma and clean technologies. No specific restrictions on these technologies have yet been announced but may well be on the way.

With the exception of quantum sensing, which is delivering real-world benefits in areas such as geolocation and meteorology, quantum computing remains largely in the theoretical stage, though the potential benefits of practical applications are enormous.

The US is significantly ahead of China in all aspects of quantum research apart from quantum communications, where Professor Pan Jianwei of the Hefei Institute of Higher Physics has registered significant progress.

If the US wished to hobble China’s efforts to become a world leader in quantum computing, it could withhold access to quantum computing hardware, error correction software (needed to correct distortions caused by noise and vibration), the ion trap technology needed to isolate individual atoms, and the dilution refrigeration technology needed to freeze individual atoms to just above zero degrees absolute.

Three firms - Finland’s Bluefors, the UK’s Oxford Instruments Nanosciences and the US company Janis ULT – currently have 70% of the global market in this latter technology. While Chinese scientists have undertaken leading-edge research in dilution refrigeration, it has not yet been significantly commercialised.

On biopharma, possible actions the US government might take include restricting access to biological materials, technical information and laboratory equipment and software used in medicine manufacture. It could also impose curbs on the transmission to China of data used to manufacture medications.

It might also put restrictions on the sale of seeds to China and ban the use of the dollar when investing in specific technologies in China. At present this is in the realm of speculation.

Implications

It is hard to be categoric about the implications of US actions to date, but some trends are beginning to become clear. The first is that US technology companies are becoming more cautious about engaging with China, and those that manufacture in China are beginning to diversify in order to spread their risk.

This is true even of Apple. However, the company remains heavily invested in China and is likely to continue to assemble the majority of its products there.

The second trend is that within the past year there has been something of a renaissance in manufacturing in the US, driven by a growing awareness of the fragility of global supply chains and by substantial government subsidies. By no means all this investment is in hi-tech products but there is a particular focus on semiconductors and electric vehicles.

This spurt of US manufacturing activity will not be a substitute for Chinese manufactures but will go some way to creating greater supply chain redundancy.

Thirdly, Chinese manufacturing, though still strongly positioned by virtue of the deep clusters of expertise developed over the past 30 years, is beginning to experience labour shortages. A particular issue of concern to the Party-state is the growing number of Chinese graduates who disdain blue-collar jobs. And from a technical perspective China remains heavily reliant on Western technologies in a variety of critical manufacturing processes.

That the Biden administration’s technology strategy has hit China hard is evident from the reactions of senior Chinese officials.

China’s top diplomat, Wang Yi, has described the US CHIPS and Science Act, which explicitly takes China as its frame of reference, as an exercise in highway robbery. Chinese technology companies are increasingly saying that the US restrictions mean they have to innovate or die. And China’s top leaders, though still seeking further Western investment, continue to take actions calculated to discourage such investment while relentlessly speaking of the need for China to develop indigenous capabilities.

Conclusion

The tech war that the US is waging against China is set to have a decisive impact on the global economy for years to come. Whoever wins the 2024 US presidential election, it is hard to foresee an easing of the pressure on China given the animus towards China across the political spectrum.

As US sanctions prompt Western firms to beware of doing business with China, globalisation and innovation risk being the collateral damage. On the upside, a renaissance in US manufacturing is unfolding, nurtured by massive government aid for advanced chip production and for the development of renewable energy.

As for China, Washington’s onslaught will not deter President Xi Jinping from pursuing his ambitions. He wants China to become the global leader in the next generations of advanced technologies; set technical standards that others must abide by; derive economic benefit from sales and royalties; and use its technological edge for national security and national advantage – just as the US has done for many decades.

But the contest to arrive at that position will be more bitter than Beijing had hoped or expected.